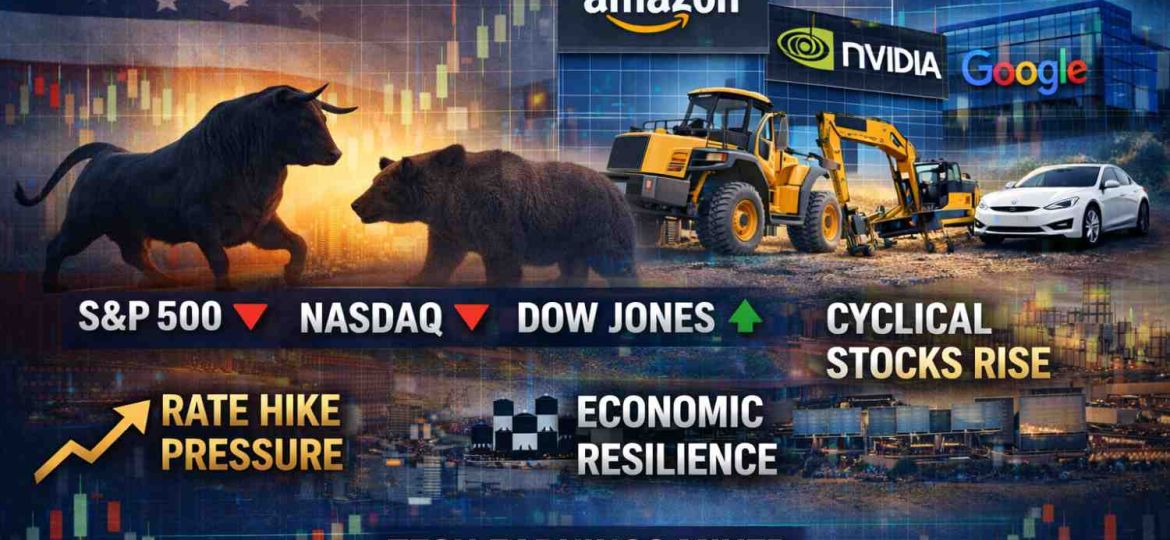

Volatility Returns as Rates and Earnings Drive Sentiment

US equities ended the week mixed and notably more volatile, as markets recalibrated expectations for Federal Reserve policy alongside a heavy slate of corporate earnings. The S&P 500 and NASDAQ Composite struggled to maintain early-week gains, while the Dow Jones Industrial Average showed relative resilience due to strength in industrials and financials. Treasury yields moved higher during the week after stronger-than-expected economic data reinforced the “higher-for-longer” rate narrative, putting pressure on long-duration growth stocks and leading to a rotation into cyclicals and value-oriented sectors.

Macro Focus: Resilient Data Pushes Back Rate-Cut Expectations

Investor positioning shifted as labour market and services data pointed to continued economic resilience, reducing the urgency for near-term rate cuts. Markets began pricing a later start to the easing cycle, which weighed particularly on high-multiple technology names. The move in yields was the dominant macro driver, reinforcing sensitivity to duration risk and compressing valuation multiples across parts of the growth universe.

Mega-Cap Technology: Divergence Emerging Within Leaders

Earnings from mega-cap technology companies drove a more selective market response compared with the broad-based rallies seen earlier in the cycle. Amazon.com, Inc. declined following its results, as investors reacted to significantly higher capital expenditure plans for AI and cloud infrastructure, which raised concerns about near-term margins and free cash flow despite continued strength in AWS. In contrast, Alphabet Inc. also traded lower, with softer-than-expected advertising trends and elevated AI investment guidance reinforcing concerns over near-term earnings pressure. The market reaction underscored a shift toward greater scrutiny on capital intensity, profitability and execution, rather than broad-based optimism around AI-related growth.

Semiconductors: Momentum Pauses After Strong Run

The semiconductor complex experienced profit-taking as rising yields and elevated positioning prompted investors to lock in gains. NVIDIA Corporation traded lower during the week despite unchanged long-term demand fundamentals, reflecting valuation sensitivity rather than a deterioration in the AI cycle. The pullback was broad across the high-beta chip ecosystem, suggesting a near-term consolidation phase following the sector’s strong multi-quarter outperformance.

Cyclicals and Industrials: Rotation Beneficiaries

Higher yields and improved confidence in economic resilience supported rotation into economically sensitive sectors. Industrial bellwethers such as Caterpillar Inc. and General Electric Company attracted buying interest, aided by strong order backlogs and continued strength in infrastructure and aerospace demand. Financials also benefited from the upward move in long-end yields, which improved net interest margin expectations.

Consumer and Discretionary: Mixed Signals on Demand

Within consumer segments, results pointed to ongoing bifurcation. Premium and experience-oriented spending remained resilient, while value-sensitive categories showed signs of normalization. Tesla, Inc. remained under pressure amid ongoing pricing competition and margin concerns, reinforcing investor caution toward capital-intensive growth stories in a higher-rate environment.

Takeaway: From Multiple Expansion to Earnings Discipline

The week reinforced a key shift in market leadership dynamics. With rate-cut expectations pushed out and yields rising, equity performance is increasingly dependent on earnings delivery, cash flow visibility, and capital efficiency. Broad multiple expansion appears less likely near term, and leadership is rotating toward companies demonstrating operating leverage, pricing power, and balance sheet strength. The near-term outlook suggests continued volatility as markets balance resilient growth against restrictive financial conditions, with stock selection likely to drive returns more than index direction.